Pulse guidance note – March 2020

~ Guidance notes for the Australian Pulse Value Chain ~ Edition 7, March 2020

Download PDF version of this report.

This global pulse update has been prepared by Pulse Australia, and the Grains Industry Market Access Forum (GIMAF), with the support of the Australia - India Council, to inform the Australian pulse value chain about the trends and drivers in the global pulse market.

The aim is to have a better-informed industry in order that grower decisions around pulse area and rotations can be made with more confidence, while the processing, trading and logistics sectors can better plan for the year ahead.

This edition of the Pulse Guidance Notes is specifically timed to assist growers with final decisions for 2020 winter planting and rotations.

Key Points:

- Recent panic buying in the Indian sub-continent not impacting demand (yet);

- COVID-19 impact yet to be felt in key markets;

- Indian Rabi crop potential reduced due to recent heavy rain and hail;

- Chickpea production in India and Pakistan likely to meet domestic demand.

COVID 19 and Pulses:

It is challenging to commence any discussion these days about anything without referencing COVID 19. So we start this Pulse Guidance Note with a view on COVID 19 and what this might mean for pulse supply and demand. Domestically, there is mild concern that the knock-on effect of the 6-8 week shutdown in China may impact chemical and fertiliser supplies. As the pandemic situation in Australia advances, there could also be delays in Australian stevedoring activities to unload replenishing supplies of chemical and fertiliser. Peak industry bodies such as NFF, GTA and GGL are assessing the likely extent of any impact on chemical and fertiliser supplies. Inoculant supplies are less likely to be impacted as many inoculants are produced locally. Restrictions on state border crossings will not impact freight of any agricultural inputs, but there can be delays in border crossings.

From an export perspective, the China shutdown has triggered a shortage of shipping containers arriving in Australia, which may impact near term export of containerised pulses. By harvest time, this issue should be overcome.

From a demand perspective, India is reporting panic buying as the country effectively went into lock down this week. The initial rush on hygiene products is now spreading to foods and workers are being encouraged to stay indoors and works from home. Similar trends are being reported in Pakistan and Bangladesh, with Governments urging citizens to cease stockpiling goods.

John Hopkins University Corona virus tracker reports the following numbers of confirmed cases of COVID 19 for the sub-continent (as at Tues 25.03.20)

- India 562

- Pakistan 1000

- Bangladesh 39

- Sri Lanka 102

However, these numbers are most likely highly under representative of the situation and combined with the challenges in instituting social distancing in these countries, social and economic disruptions in these key pulse markets is likely to escalate rapidly.

The impact of panic buying is yet to translate into any appetite to replenish stocks, indeed, reports are of the opposite, with sub-continent buyers reported to be reluctant to engage in any trade with the dark cloud of uncertainty overhead.

Enough on COVID 19- it is what it is, and we have to work with what we have.

Sub-Continent Seasonal Update:

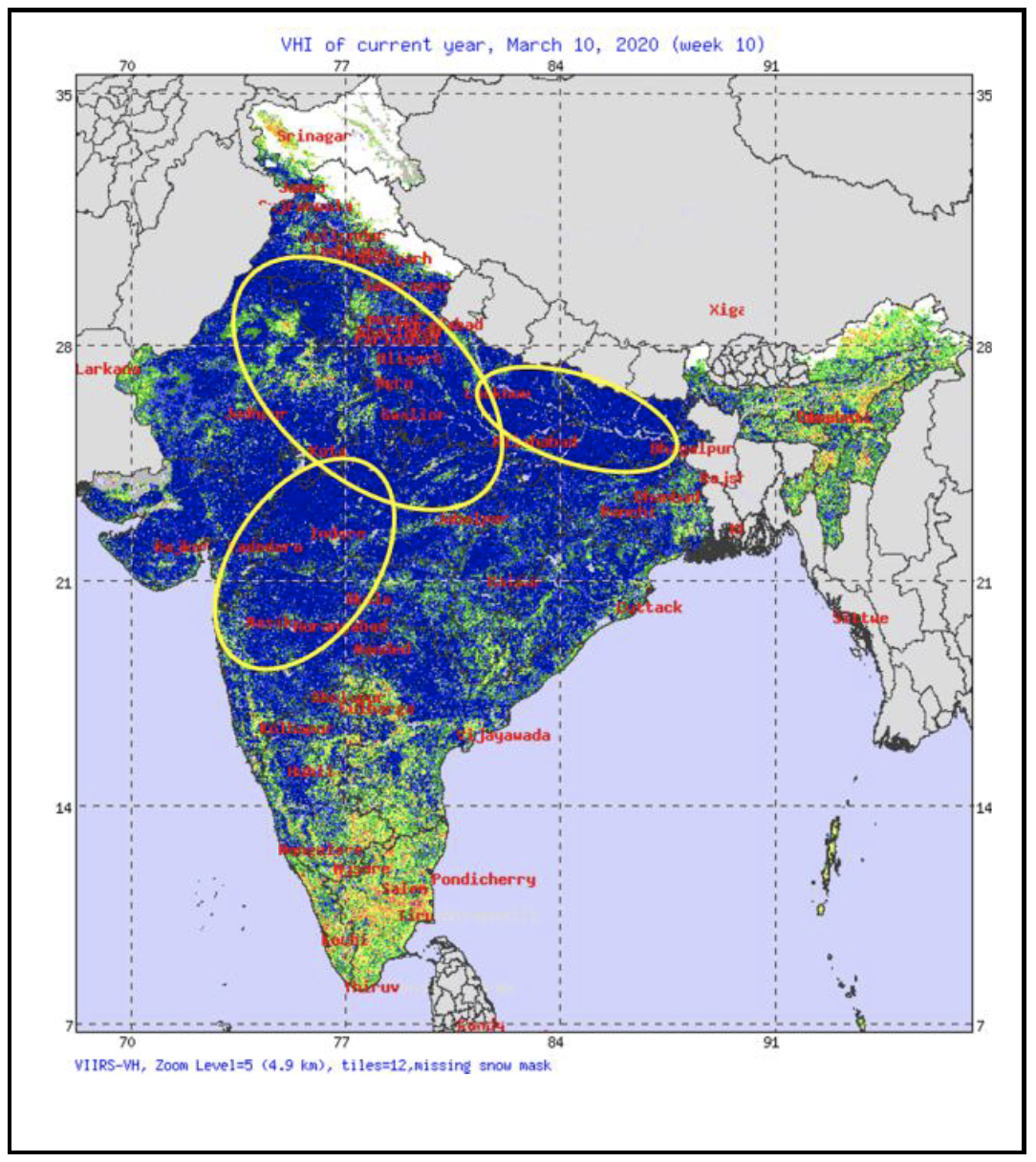

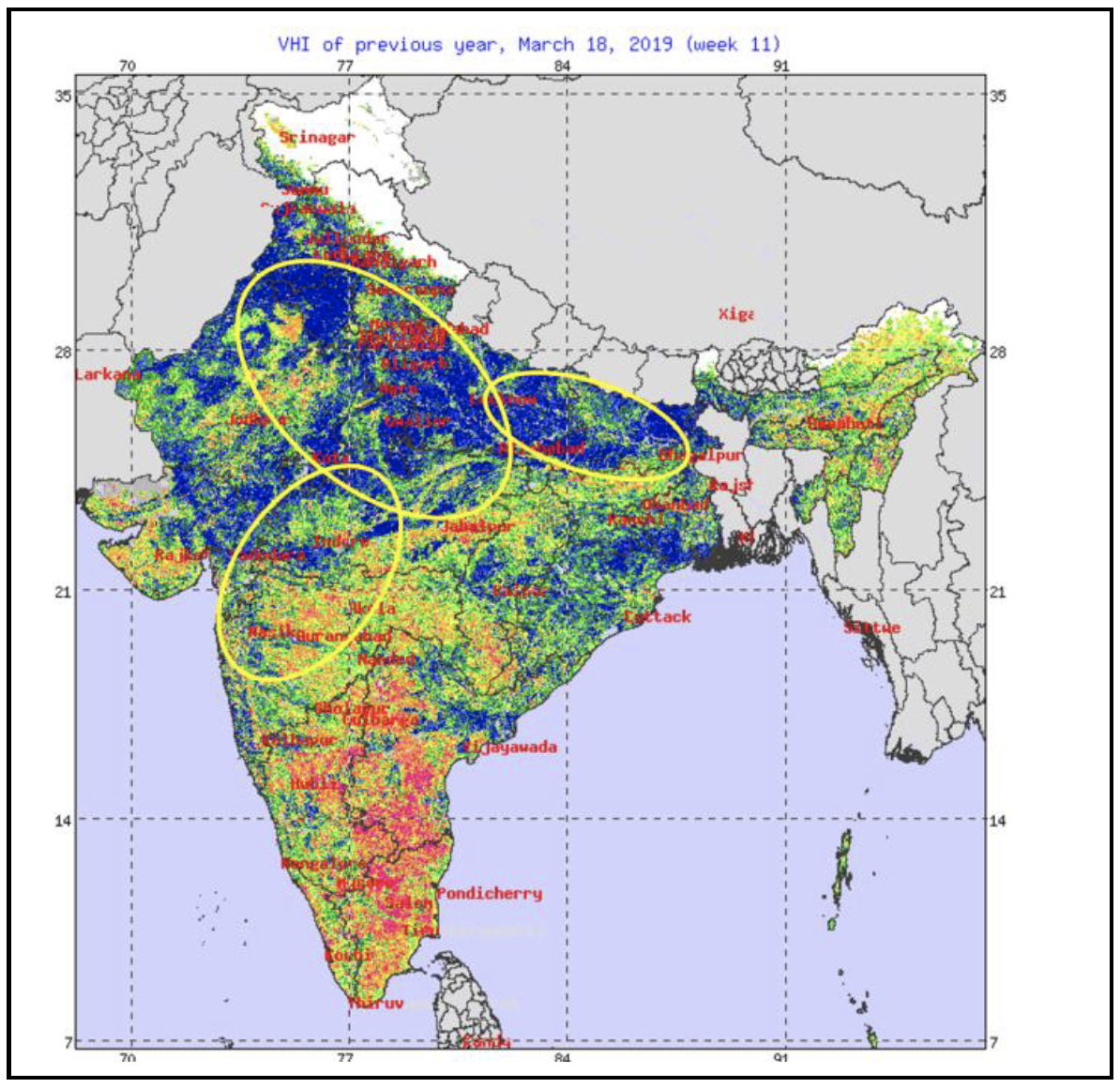

The key single determinant on the fortunes of the Australian pulse industry is the production prospects for pulses in the sub-continent. The rabi season (chickpeas, lentils, peas) is now approaching harvest and by all accounts the season has been good in India, with a cool finish and no moisture stress.

The vegetation index maps (below) demonstrate the improved conditions vs last year for the major pulse growing regions (circled in yellow).

Indian Vegetation Index- March 18, 2020

Indian Vegetation Index- March 18, 2019

Source: National Oceanic and Atmospheric Administration

Source: National Oceanic and Atmospheric Administration

However, reports last week of heavy rain and hailstorms in March may reduce yields significantly. So far this month, rains have been 776% above normal in Uttar Pradesh, 701% above normal in Haryana, 446% above normal in Punjab, 456% above normal in Rajasthan and 300% above normal in Madhya Pradesh. Wheat, mustard and potato seemed to have suffered most with chickpeas having suffered less.

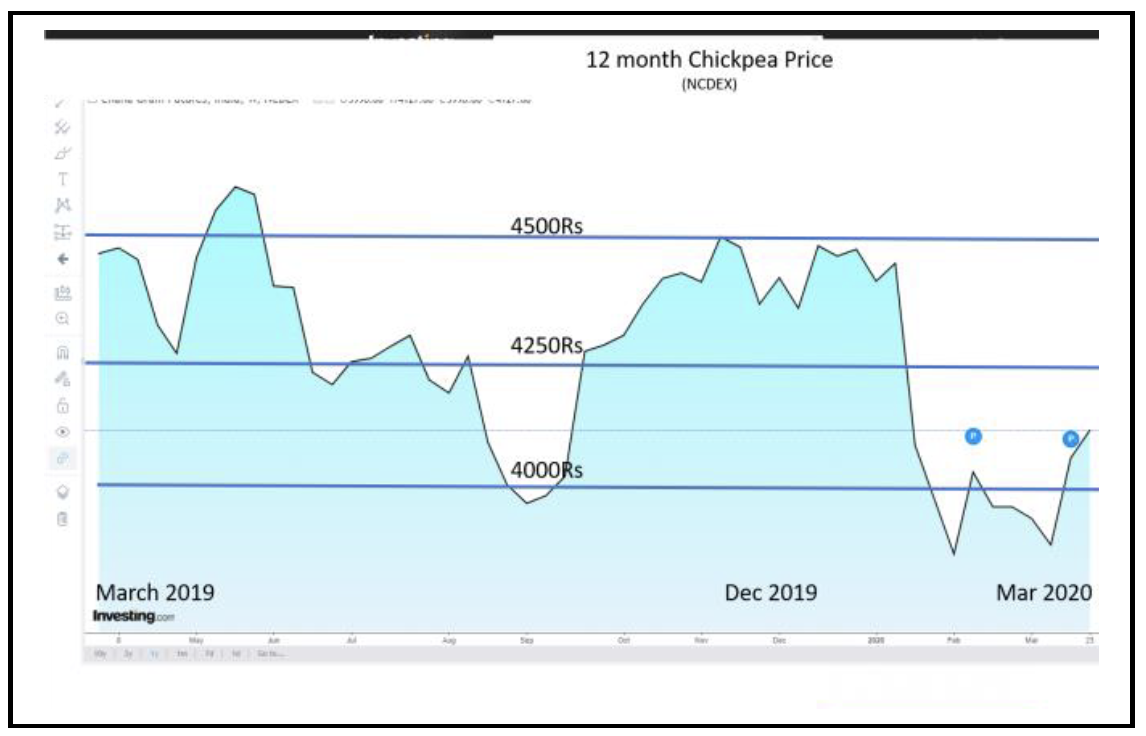

The chickpea harvest prior to accounting for any storm related loss was forecast to be 11.2 mmt. Typically, any production of chickpeas in excess of 10mmt will indicate minimal imports will be needed.

The price for chickpeas in India has come off recent highs as the crop prospects brightened but have regained recently, most likely in response to concerns over yield loss through storms.

Meanwhile in Pakistan, the chickpea crop is also approaching harvest and with a forecast 600,000 tonnes, there is expected to be limited, if any, demand for imported chickpeas.

Consequently, Australia’s prime destination market for chickpeas is likely to be Bangaldesh, with a max potential of circa 200,000t.

With trade restrictions applying to chickpeas, peas and lentils into India, faba beans from Australia are gaining favour, with nearly 11,000 tonnes shipped from last harvest. The Indian propensity to blend flours has seen (cheaper) faba bean flour blended with (more expensive) chickpea flour in a proportion that does not materially impact performance.

Global Picture:

Globally, the world is slowly eating through supplies of lentils, so prices are edging up slowly, but trade restriction into India are limiting overall marketing opportunities to Bangladesh, Sri Lanka, Egypt and Pakistan.

Egypt has taken 20,000 tonnes across two bulk shipments of Australian faba beans along with over 50,000t of containerised beans, which is broadly in line with typical annual purchases (up to January each year). Egyptian demand remains reasonably consistent, and with the easing of drought conditions in Australia, more of the Australian crop can be expected to be destined for Egypt.

Bottom Line

The unprecedented uncertainty in the world driven by COVID-19 is impacting both individual behaviour as well as group behaviour. The impact of the uncertainty is yet to clearly play out in the pulse market, but underlaying fundamentals will remain.

The generally good rabi pulse production in India and Pakistan this season will mean their need for imported pulses will be modest. For India, the promising production will also mean there is little need to soften existing trade restrictions.

Trade patterns are therefore likely to mirror that of the last 18 months:

Market and Main Crop

- Bangladesh – Chickpea/Lentils

- Egypt – Faba

- Sri Lanka – Lentils

- Pakistan – Chickpeas

- India – Lentils

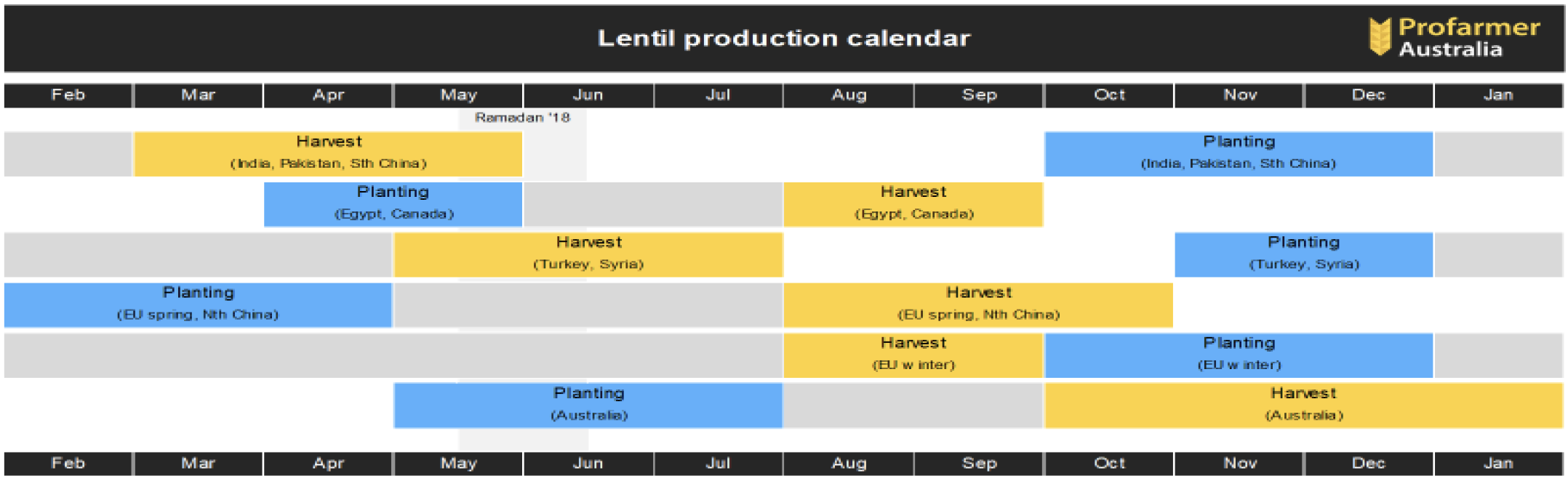

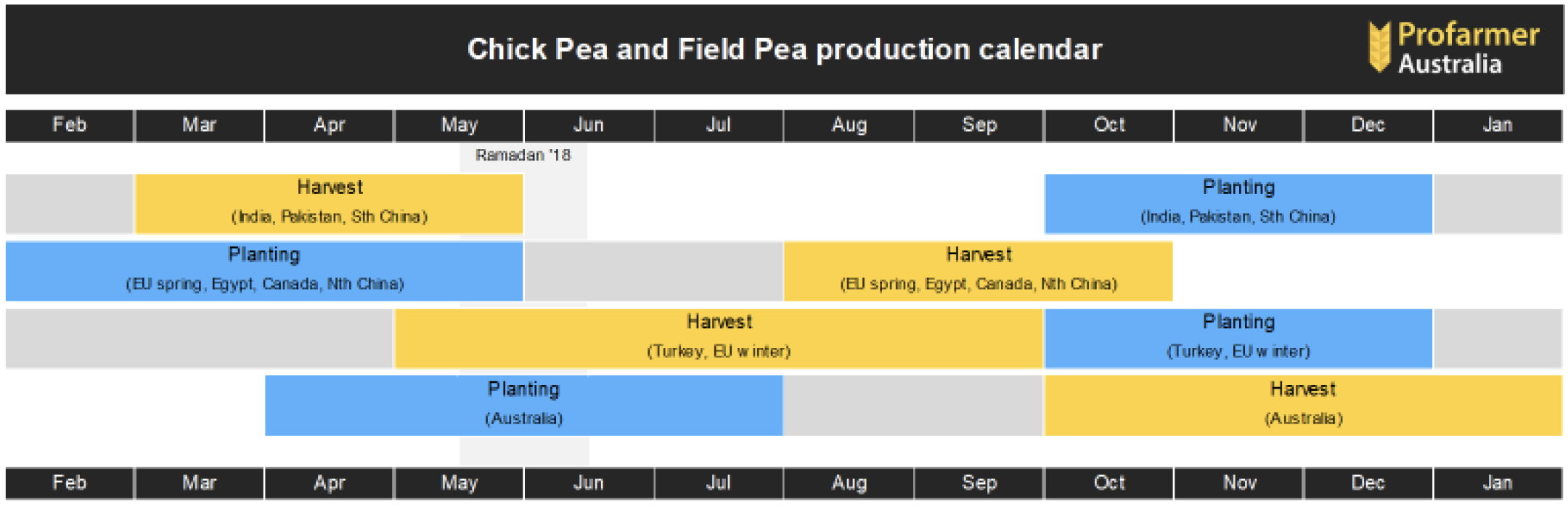

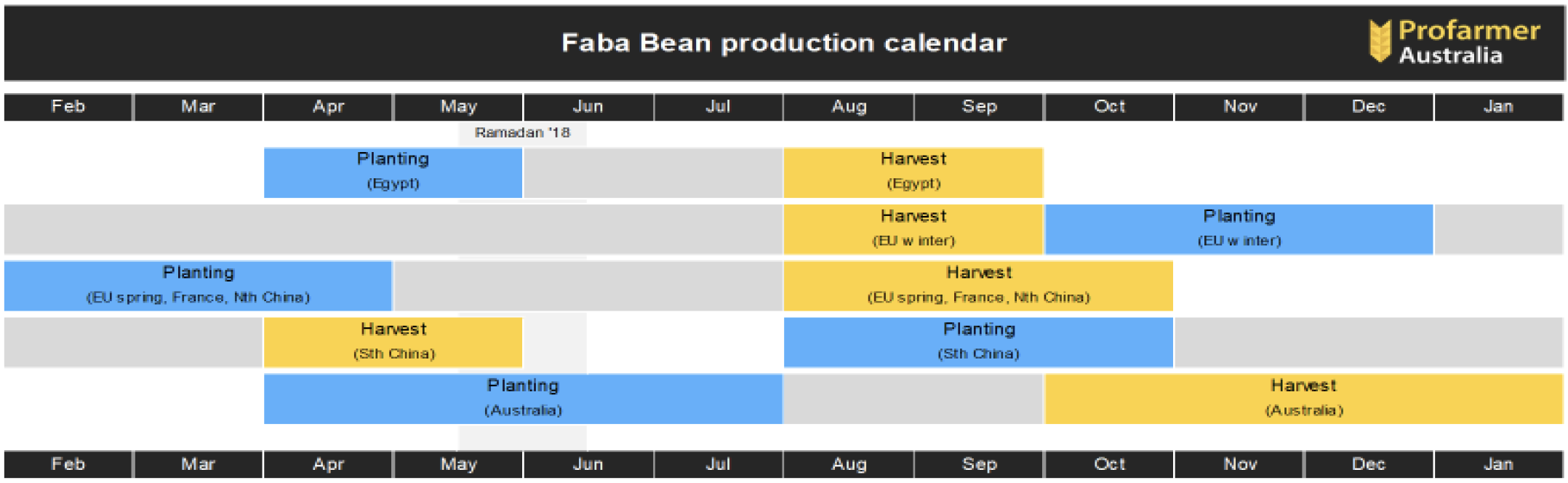

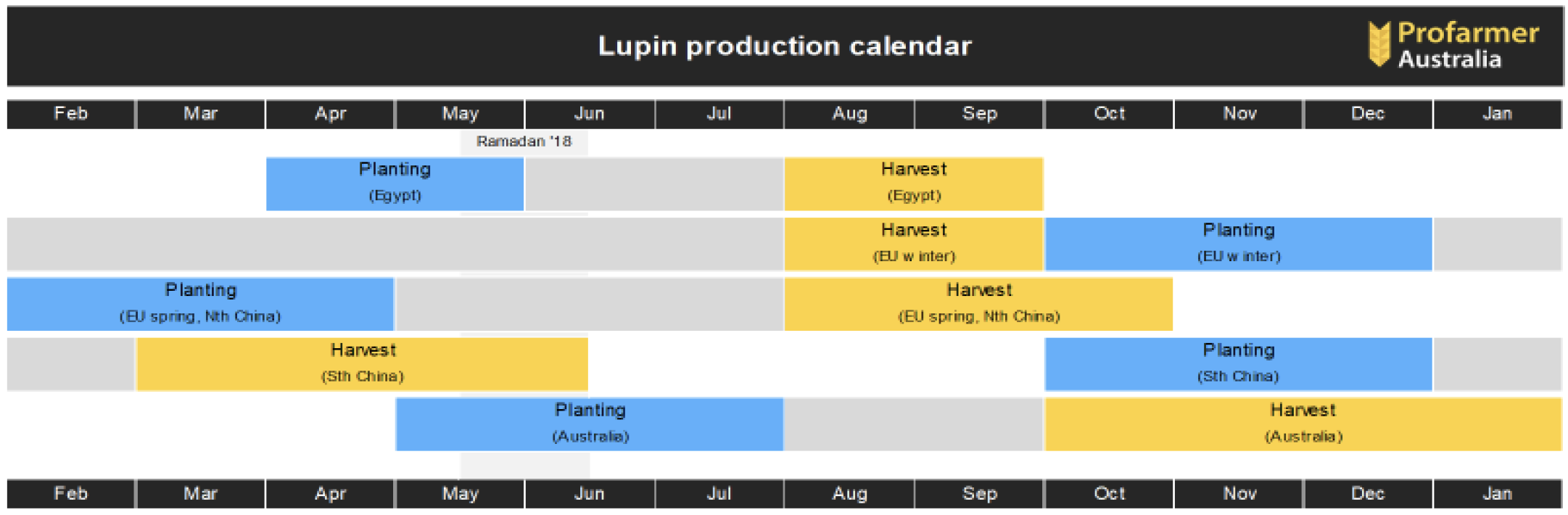

Global Pulse Production Calendars

This report has been compiled by GIMAF and Pulse Australia, with the support of Australia-India Council. Information has primarily been sourced from published reports and data.